China Flexes Critical Mineral Dominance as US Tariffs Reshape Global Energy

Plus, what an end to Russian sanctions could mean for the industry, how targeting US state policies could slow the clean energy transition, and the rising role of the Arctic frontier

This week we recap the ripple effects of the US tariff frenzy on the global energy sector and China’s response by imposing export restrictions on critical minerals including rare earth elements vital to US energy and defense industries. We also examine how an executive order targeting state-level climate change and energy policies could affect the energy transition. Finally, and more broadly, we explore the emerging trends and ‘what ifs’ around lifting sanctions on Russia’s energy sector and how record-low Arctic sea ice levels are fueling the geopolitical race.

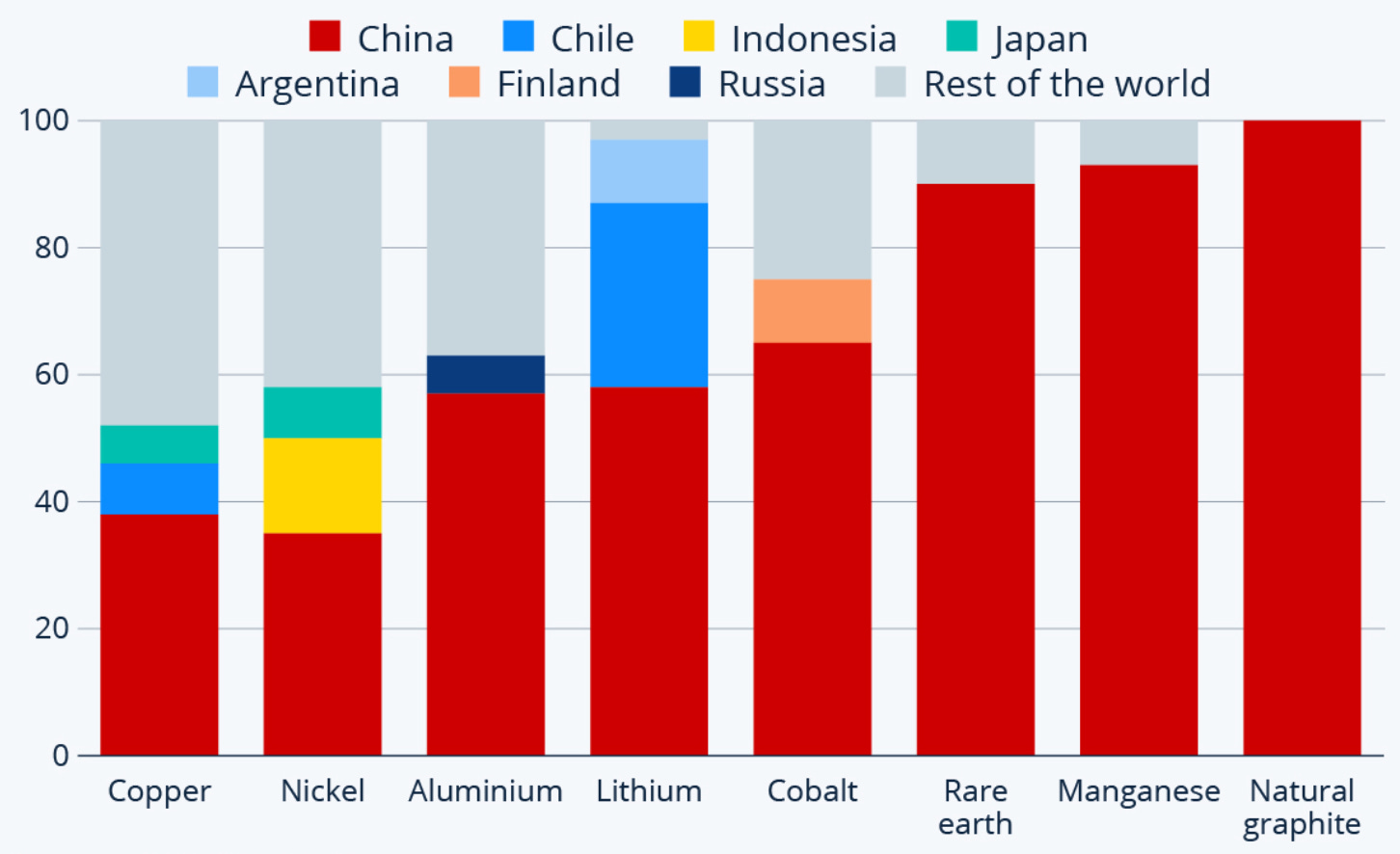

China institutes export restrictions on critical minerals to the US

Driving the News: China’s Ministry of Commerce has imposed restrictions on the export of seven specific rare earth elements (REEs) and specialty magnets to the US in direct response to increased tariffs and the escalating trade war (NY Times).

While not an outright ban or monetary tariff, the export restrictions now require any Chinese entity seeking to export heavy rare earth metals and rare earth magnets to the US to obtain a special license from the government.

Why it Matters: The US has long been wary of China’s monopolies across the global critical mineral supply chains, and last week’s actions demonstrate that Beijing is clearly willing to leverage this position as a geopolitical tool.

The Context: These most recent export controls build on top of an emerging trend by Beijing to flex its position as the linchpin of the global critical mineral industry.

Concern about China’s role in controlling the global supply chain dates back to 2010, when China first halted the export of REEs to Japan after it detained a Chinese fishing boat captain.

The US has taken steps toward addressing its exposure in recent years, including through the 2024 National Defense Industrial Strategy, which set a target for developing a mine-to-magnet REE supply chain by 2024, and over $439 million in DOD investment into domestic supply chain development.

The Intrigue: On December 1, 2024, China introduced a new framework for regulating dual-use products (those materials and products that can be used in both civilian and military applications), followed soon after by an export ban and restrictions on several critical minerals to the US in response to the expansion of technology restrictions on China (S&P Global).

The Impact: Unlike other commodities such as oil and gas that have an immediate impact on prices and energy availability, the potential halting of these critical minerals would have a more delayed effect.

In the immediate term, there is likely to be a pause on exports of restricted materials to the US as the Chinese government sets up its licensing system and companies apply for approval to continue trading. While some US defense companies and the DOD do have a limited stockpile of rare earths to draw on, these reserves are only enough to meet a few months’ worth of demand (CSIS).

Longer term, it remains to be seen how hard China will squeeze the US with critical mineral limits. If China does in fact move forward with restricting supply, there would be major impacts on key US sectors including the national security and defense, energy, and automotive industries.

The Geopolitics: While many countries are investing heavily to reduce their exposure to Chinese-controlled critical mineral supply chains, the reality is that China remains decades ahead, with production capacities that will be extremely hard for the rest of the world to catch up to.

Initiatives are currently underway in Australia, Brazil, Japan, Saudi Arabia, South Africa, the US, Vietnam, and elsewhere to increase the extraction and refining capacity for REEs and other critical minerals.

Looking Forward: While the export restrictions are a major first step, China has left itself plenty of room to escalate. The order is limited to only a select set of minerals and stops short of actually banning any minerals. As the US continues to ramp up its trade war and further technology restrictions, China may take more severe action.

US ‘Liberation Day’ tariff announcements impact global energy sector

Driving the News: On April 2nd, President Trump declared “Liberation Day” as he unleashed a flurry of tariffs on US trading partners around the world, impacting markets and industries across the board.

In the days since, a chaotic combination of bilateral negotiations has led to a 90-day pause on most tariffs, leaving in place a new 10% global tariff, a spiraling set of retaliatory duties between the US and China, and a global unease about the future of international trade (JP Morgan tariff timeline).

The Energy Angle: From the outset, strategic exemptions were made for the energy sector—as well as for copper, pharmaceuticals, semiconductors, lumber, and critical minerals—yet the impacts on the industry have still been substantial (CSIS).

Oil markets slumped, with prices falling sharply on the double blow of reduced economic outlook and announced OPEC production increases (Reuters). Concerns are also mounting within the LNG industry about targeted retaliatory tariffs.

The US power sector is also highly exposed to tariff impacts, with an estimated 38% weighted average tariff rate on electrical equipment (per original tariff announcements) and high rates on other key materials for the sector such as plastics, glass, and iron—all of which could add to inflationary pressures as utilities pass rising costs on to consumers (Wood Mackenzie).

Tariffs on steel, aluminum, other materials, and equipment are also likely to push up the costs associated with producing oil and gas, building LNG facilities, and deploying renewable energy.

Internal Tensions: Within the energy sector, the costs associated with tariffs highlight a key tension between the Trump Administration’s trade strategy and its own targets of boosting domestic energy production and reducing consumer costs.

Lower oil prices have substantially undermined the Trump Administration’s “Drill, Baby, Drill” agenda. Prices have already fallen below the level that many US shale producers need to break even, and the administration’s target of $50 per barrel would lead to mass idling of rigs and selloffs (Financial Times).

The policy ‘whiplash’ is also worrying to the sector, making it more difficult to invest in projects with the multi-year to decade-long time horizons typical of the energy industry.

The Geopolitics: As the world continues to seek out the energy sources of the future, the broad use of tariffs (in concert with the myriad other anti-renewable energy policies coming from the current administration) could drive a broader realignment that excludes the US as China steps in as the global supplier of clean energy technologies and materials.

How an end to Russian energy sanctions could reshape the industry

What to Watch: As talks of ending the war in Ukraine continue to evolve, the prospect of reducing or eliminating Russian sanctions on energy exports is increasingly on the table.

The Context: As one of the primary engines of the Russian economy, the country’s oil and gas sector has been the target of Western-backed sanctions starting in 2014 following the annexation of Crimea, and escalating substantially in 2022 with the invasion of Ukraine.

Prior to the 2022 invasion, Russia was one of the largest exporters of fuel oil to the US and a critical supplier of oil and gas to the EU.

Since then, however, a coalition of Western countries has implemented a range of export controls including price caps, blocking Russian entities from SWIFT and other global financial services, and bans on imports that have effectively eliminated Russian exports to key markets around the world. The EU is set to publish its plan for completely phasing out Russian oil and gas by early next month (Bloomberg).

One Big Question: Should the war come to a close, those countries that have implemented strong sanctions and export controls will need to decide whether those instruments should remain in place or be lifted, allowing Russian energy back into the global markets.

Unblocking the restrictions would make it easier for Russian companies to begin transacting in dollars again and resume the operation of a large number of tankers, reducing costs and increasing earnings for the Russian energy sector and the state (Reuters).

The Intrigue: Since the invasion and the subsequent isolation from the global market, however, the Russian economy has shifted to focus on military production and shorter-term stability rather than long-term growth.

As CSIS reports, “The substantial investment in military infrastructure and the prioritization of defense industries indicate that Russia is preparing for prolonged geopolitical tensions, with an economy increasingly centered on military capabilities.”

As a result, the Western coalition will need to prepare for how to contend with a militarized economy in Russia even post-war, and consider how the resumption of energy revenues may risk financing an increasingly confrontational adversary.

Looking Forward: For the foreseeable future, Russia is likely to continue selling its oil and gas to India and China, which have become its top buyers. A return of Russian volumes to global energy markets could depress prices, especially in Europe, while reigniting tensions among countries that pushed for long-term decoupling from Russian energy.

US executive order targeting state energy policies

Driving the News: Last week, the Trump Administration issued an executive order directing the Attorney General to identify and stop any state laws pertaining to issues of climate change and—by extension—clean energy.

The order, titled Protecting American Energy from State Overreach, contends that states are enacting “burdensome and ideologically motivated ‘climate change’ or energy policies that threaten American energy dominance and our economic and national security” (White House).

The Context: Per the EIA, “Over half of states have either required standards or have established voluntary goals, targets, or objectives for renewable or clean energy supply within specific timeframes.”

The Impact: Although the Executive Order only directs review of the laws and does not directly challenge them, it does set up the framework for litigation and the withholding of federal funds (Columbia Sabin Center).

With preemption litigation hampered by the lack of existing federal laws on related topics, the potential to withhold federal funding from states deemed noncompliant is a much more near-term risk.

However, many programs such as state-level cap-and-trade and California’s Low Carbon Fuel Standard have already survived extensive constitutional challenges by the federal government, potentially limiting the options for restricting such policies going forward (Holland & Knight).

The Geopolitics: Although a domestic issue on its face, US states have played an increasingly important role in forwarding climate change policy and maintaining the momentum for renewable energy markets as the federal government has stepped back (including exiting the Paris Agreement for a second time).

In a recent paper published by the Carnegie Endowment arguing for a clean energy foreign policy as a means for cultivating geopolitical advantage, Bentley Allan explains that “technological leadership and manufacturing capacity lies at the heart of geopolitical competition today.” By losing the race for future energy technologies, the paper argues that the country will fall behind, particularly as China does the opposite in pursuing strategic investment in clean energy supply chains and products.

Anecdotally, under the current administration, state policies (along with corporate policies) will remain the key drivers of clean energy industry development and deployment. Hindering or eliminating such policies could risk undermining the US position as a technology leader in the space.

How a melting Arctic is opening a new geopolitical frontier

What to Watch: This past March marked the fourth consecutive month with record low sea ice in the Arctic, furthering expectations that some parts of the region will be ice free within a decade. As Rebecca Pincus, former director of the Wilson Center’s Polar Institute, puts it, “the trend line is in one direction” (Financial Times).

Why it Matters: As the polar regions continue to warm at a much faster rate than other latitudes, the race for control of strategic shipping routes, increased military presence, and energy resources is accelerating. This issue in particular sits at the direct confluence of climate change, energy, and international affairs as countries look to the future in a warmer world.

The Context: Melting sea ice in the Arctic is opening up previously impassable areas to new mineral deposits and shorter trade routes—including the Northern Sea Route, which passes through Russia’s Exclusive Economic Zone but is claimed by Moscow as sovereign territory, and the Northwest Passage, which runs along the coasts of the US and Canada.

The Geopolitics: The eight members of the Arctic Council (plus one self-proclaimed “near-Arctic state” as China puts it) are already vying for position and influence in the region, leading to great power tensions and a build-up of resources.

Russia has been intensifying its militarization of the region in recent years, with its largest naval fleet located directly along the Northern Sea Route on the Kola Peninsula. Many analysts foresee an end to the Ukraine war leading to even further military focus in the Arctic, particularly as the country has shifted toward a wartime economy (as discussed above).

China is investing heavily in Arctic energy exploration and building its own military presence, including through joint exercises with Russia. Two major Chinese energy entities—the China National Petroleum Corporation and the China National Offshore Oil Corporation—are partial owners in Russia’s largest LNG projects, Arctic 2 and Yamal, and Presidents Xi and Putin last year announced a joint commission to develop the Northern Sea Route as part of the country’s “polar silk road” (RAND).

The US has resumed Cold War-era presence in the region, partnering with Norway’s military to train an initial 8,000 NATO troops in the “art of cold-weather warfare” and speaking openly about the strategic need to annex Greenland (an ally which notably already allows major US military presence on the island), though it is unclear how serious the US is in pursuing that strategy. Last year the US also published its first update to its Arctic Strategy since 2019, which highlights a need to engage with allies and pursue a “monitor-and-respond” approach to the region (US DOD).

The European Union has also voiced interest in engaging in the Arctic as a “geopolitical necessity”, with Norway seeking to ramp up oil and gas exploration projects and the development of renewables to power Arctic communities as a key strategic goal for the bloc.

The Energy Angle: As a direct byproduct of global warming, how quickly the trade routes and resources in the Arctic become accessible will depend in large part on the speed with which the world decarbonizes. Under current emissions pathways, the region could become ‘reliably’ ice-free in summer by 2050.

Dive Deeper: Over the last two months, The Financial Times has published a great four-part deep dive covering the “new geopolitical and commercial power struggle” taking shape in the Arctic.

Image Sources:

Investment Monitor, Getty Images

Statista, UNCTAD, OECD