DOE Commits a New $2 Billion Toward Battery Component Manufacturing

Plus BP's reversal back to fossil fuels, Europe's ban on Russian Diesel, and the Arguments for Defining Green Hydrogen

DOE Makes $2 billion Conditional Loan Commitment to Battery Component Manufacturer Redwood Materials

DRIVING THE NEWS: DOE’s Loan Programs Office announced a $2 billion conditional loan to Redwood Materials for the construction and expansion of a battery materials production facility in McCarran, Nevada (see press releases from Department of Energy and Redwood Materials).

The funding will allow Redwood Materials to expand production of its battery components to support up to 1 million EVs per year. The company has supplier agreements with Ford, Toyota, Volkswagen, Volvo and Panasonic; the last of which will use Redwood’s components to produce EV batteries for off takers like Tesla (NY Times).

Per the DOE, “[this] project marks a significant step towards meeting the Biden administration’s target of making half of all new vehicles sold in 2030 zero-emissions vehicles, including battery electric, plug-in hybrid electric or fuel cell electric vehicles.”

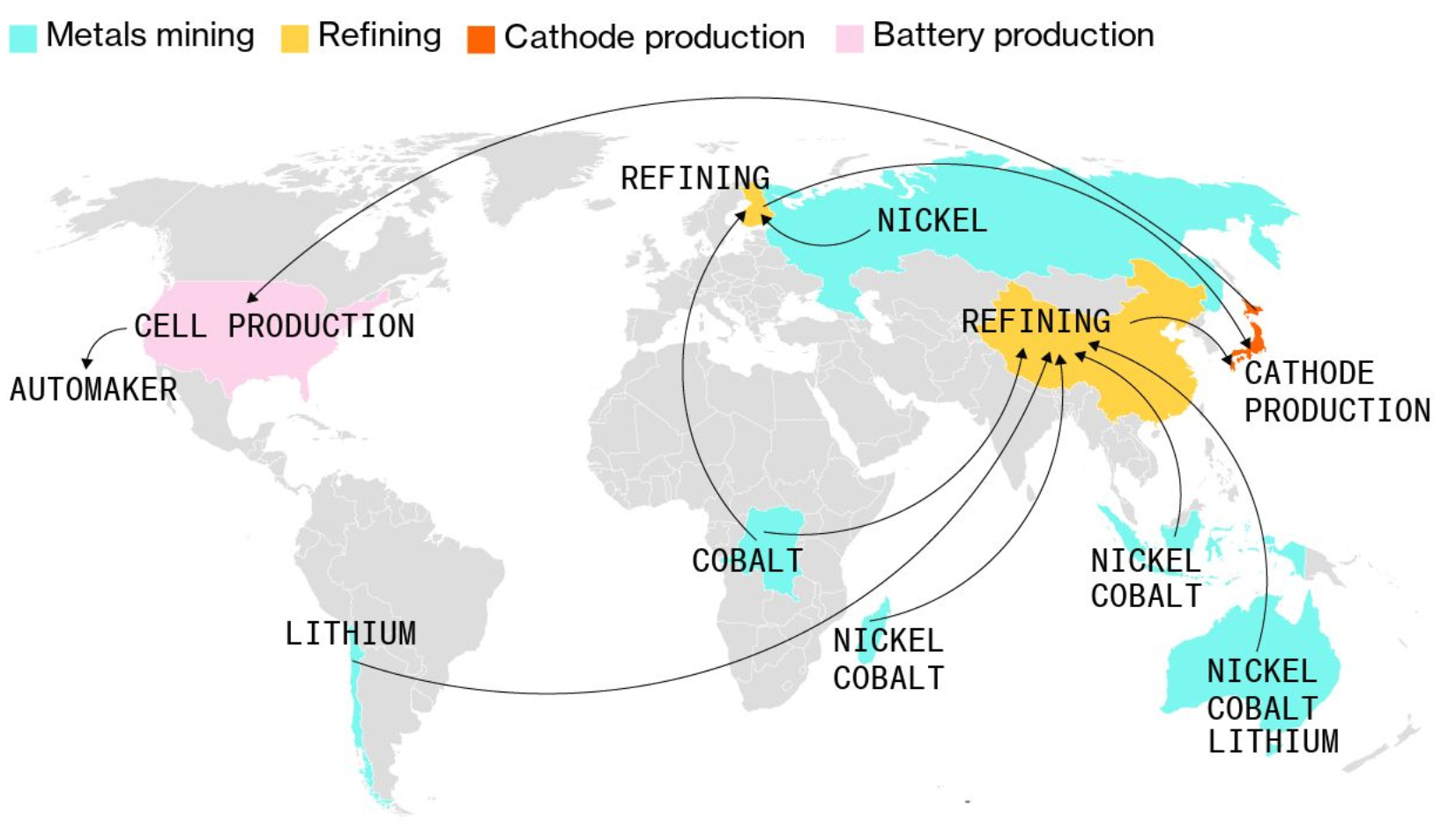

WHY IT MATTERS: The facility will be the first in the country to support production of anode copper foil and cathode materials; key ingredients for lithium ion batteries that are currently only produced in Asia (see supply chain map below). As DOE points out, “onshoring is a key part of the critical materials supply chain” for the growing EV sector.

Figure 1: Illustration of the current supply chain for US battery components that Redwood Materials hopes to consolidate (Source: Bloomberg)

Founder of Redwood Materials J.B. Straubel explains: “It is the very tangible beginning of a US supply chain for battery materials, and we’ll be ramping that up for quite a long time to come.” (Bloomberg)

Redwood plans to quickly follow the Nevada project with a second plant currently being constructed in Charleston, SC (not included in the DOE loan) with the goal of supplying America’s emerging “battery belt”, which stretched from Michigan to Georgia.

INVESTMENT TREND: This is the fourth commitment in six months from LPO’s Advanced Technology Vehicle Manufacturing loan program. The office was revived under the Biden administration and given new loan authority through the IRA. We are likely to see many more such investments in domestic cleantech in the coming months and years.

Prior to Redwood, the LPO recently authorized conditional loans of $102 million to Syrah Technology’s processing facility to produce critical battery materials, $700 million to the Rhyolite Ridge lithium carbonate mining project in Nevada, and $2.5 billion to Ultium Cells, battery manufacturing JV between General Motors and LG.

CIRCULAR ECONOMY: The facility will use both new and recycled feedstocks to produce roughly 36,000 metrics tons of battery-grade copper foil per year. Recycled materials will come from consumer electronics (e.g. cell phone batteries, laptops, power tool, etc.), helping create a circular supply chain in the US.

BP Reverses Course, Plans to Increase Oil and Gas Production

WHY IT MATTERS: The recommitment to longer-term oil and gas production, only two years after BP announced its new business direction away from O&G, demonstrates just how rapidly the mindset on the longevity of fossil fuels has shifted given the changing geopolitical situation.

BP’s recently released 2022 annual report shows a $10 increased from last year in its assumed Brent oil price for 2030 to $70 per barrel. That high of a price through the end of the decade would keep the business case for O&G stronger, slowing the oil majors’ transition to low carbon alternatives.

DRIVING THE NEWS: BP last week announced a major reversal to its transition plan. The company now intends to continue increasing investment in O&G production through the end of the decade.

In announcing the reversal, CEO Bernard Looney provided context for the decision: “The conversation three or four years ago was somewhat singular around cleaner energy, lower-carbon energy… Today there is much more conversation about energy security, energy affordability.”

Most dramatic is the increase of investment into O&G production by an average of $1 billion per year through 2030 ($8 billion cumulative increase) to “help meet demand for secure supplies [while] generating additional earnings that can further strengthen BP and support investment in its transition.”[1]

These investments will target “short-cycle fast-payback opportunities with lower additional operational emissions.”

In the same announcement, the company also committed an equal increase in investment into transition growth engines (TGE)[2]: an average of $1 billion per year through 2030. This brings total TGE investment to $7-9 billion per year in 2030 for a cumulative investment 2023-2030 of $55-65 billion.

THE CONTEXT: Just two years ago, in 2020, Bernard Looney took over as CEO of BP and announced that the company would pivot to investing heavily in renewables such as solar and wind while reducing its O&G production by 40% by 2030.

The New York Times notes that the valuation of oil companies that have embraced energy transition investments into renewables, including BP and Shell, lag behind American rivals like Exxon Mobil and Chevron that have remained focused on oil and gas. Investor pressure likely played a role in BP’s decision.

Notably, this reversal is reminiscent of the last time BP attempted to instigate a transition away from its fossil fuels business, only to be forced to drop the “Beyond Petroleum” slogan and return to production partly due to the financial pressures of the 2010 Deepwater Horizon oil spill.

DIVE DEEPER: See BP’s press release for more information on the specific investments and expected outcomes, and its Fourth Quarter and Full Year 2022 Results report for a look back on the last year. Also Professor Jason Bordoff was quoted on the issue in this Wall Street Journal article.

Europe’s Ban on Russian Diesel Goes Into Effect

DRIVING THE NEWS: The EU’s ban on refined petroleum products from Russia went into effect last Sunday, Feb 5th, halting roughly 600,000 barrels of diesel that Russia had been providing to the EU every day (Bloomberg).

Many EU countries have been stockpiling the fuel in recent months ahead of the ban, hoping to reduce the price shock of a fuel critical for a wide range of industries.

In addition to the ban on seaborne imports, the EU in partnership with the G7 governments will also move to implement a $100 per barrel price cap on Russian diesel and $45 cap on oil products such as fuel oil (World Economic Forum).

“We must continue to deprive Russia of the means to wage war against Ukraine,” tweeted EC President Ursula von der Leyen, adding, “With the G7 we are putting price caps on these products, cutting Russia’s revenue while ensuring stable global energy markets.”

THE RESPONSE: Angry with the continued bans and price caps, Russia last week announced a 5%, or 500,000 bpd, voluntary output reduction of crude oil in March, with Russian deputy prime minister Alexander Novak saying, “this will contribute to the restoration of market relations” (BBC).

Despite the earlier bans, Novak says that Russia has been able to find buyers for all of its output regardless of the sanctions. Russian daily production has remained high throughout 2022 despite efforts by the West to curb sales:

Figure 2: Russian saw only a small dip in monthly crude oil production following its invasion of Ukraine last year (Source: Statista)

LOOKING FORWARD: According to Bloomberg, Russia does not anticipate major disruption to its exports, with diesel exports expected to hit 730,000 bpd this month (its highest since the start of 2020). It will remain to be seen, however, how easily Russia can enter new markets.

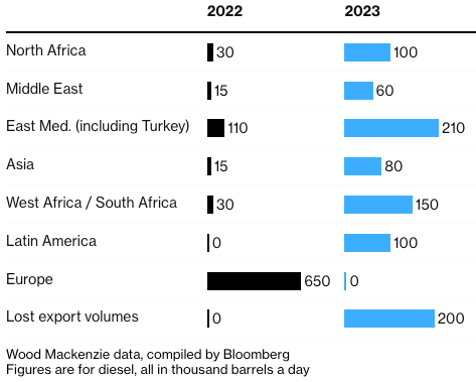

Russia will no doubt look for alternative buyers of its products in the coming year. Novak said this morning that Russia plans to sell 80% of its oil exports to “friendly” countries in 2023 (those that have not sanctioned Moscow) (Reuters). Wood Mackenzie and Bloomberg compiled a useful chart of where that diesel may go:

Figure 3: Russian diesel supplies are likely to find their way to markets in the Middle East, Africa, and Latin America, though not without major lost export volumes (Source: Bloomberg)

The Kremlin is likely hoping for a smooth supply shake-up in which current global suppliers shift to Europe and leave old markets open to Russia, though its is unclear how quickly that can happen.

DIVE DEEPER: A great piece from the Financial Times on how Russia is leveraging Iran’s “ghost fleet” to keep its oil exports flowing.

Defining Green Hydrogen Will Set a Key Precedent

WHY IT MATTERS: As the nascent green hydrogen industry gets underway in the US supported by billions of dollars in subsidies, defining what specifically constitutes “green” will have major ramifications for what projects get funded.

How the US ends up defining what qualifies as “green” hydrogen at this early stage will also likely have ripple effects to the global hydrogen industry. Early movers like the US and EU will wield outsized influence in setting rules that international suppliers will need to follow to serve these markets.

THE CONTROVERSY: In the US, the current battle is based on how projects producing hydrogen from grid electricity can qualify as “green” by purchasing renewable energy credits.

Between the IRA and IIJA, there are billions of dollars slated to support clean hydrogen projects. The IRA bases its production tax credits on the carbon intensity of the hydrogen produced (measures in kgCO2e/kgH2), but it remains unclear what that production intensity is based on. The onus currently sits with the US Department of the Treasury, which is working to finalize its rules in the coming month.

Rebecca Kujawa, chief executive of NextEra Energy Resources which is arguing for more relaxed standards, says, “If you end up having an uneconomic green hydrogen product relative to alternatives, there will be no market adoption… It’s truly an industry that is either waiting to get off the ground or will be dead on arrival, depending on what the Treasury ultimately determines.”

THE DETAILS: At the core of the argument is whether a hydrogen production facility that uses grid electricity and purchases renewable energy credits (RECs) to qualify as green must match hydrogen production to renewable production on an hourly basis, or on a much more relaxed monthly or annual basis (Wall Street Journal).

BP, Shell, and NextEra argue that they should be able to purchase RECs and only match on a monthly or annual basis. Hourly matching would force production halts when renewables are not producing, which they argue would greatly reduce the commercial viability of projects.

The counter argument, led by Vestas and Intersect Power, argues that hydrogen producers should have to prove their clean designation by matching renewable generation on an hour-by-hour basis and make sure the renewable project is located in the same region. Otherwise producers cannot claim to be clean, particularly in areas with dirtier grids.

REMEMBER BACK to last year’s EU Taxonomy debate on whether to include nuclear and transitionary natural gas as clean energy. While the specifics of the debates are unrelated, they both highlight the consequential nature of seemingly obscure bureaucratic designations that can end up being the difference of billions of dollars in funding access in the energy sector.

ICYMI: Bordoff and Tongia Debate the Necessity of Coal in Developing Countries’ Growth

In a recent piece published in the Wall Street Journal, Professor Jason Bordoff makes the case that developing countries can reach their economic growth targets without coal. On the other side Rahul Tongia, senior fellow at both the Centre for Social and Economic Progress in New Delhi and the Brookings Institution, argues that coal is necessary to reach growth targets.

Dr. Tongia points out the need to meet desired economic growth with a parallel increase in energy supply. In many developing countries, coal is the resource most available. Historic deployments of renewables to date do no keep pace with needed growth. At the same time, the energy storage necessary to deal with intermittence pushes the price of renewables well above coal in many countries. He also points out the importance of industry in many developing countries, and the inability to power these sectors with electricity alone. While Dr. Tongia accepts the ability to slow the growth of coal with renewables, he does not see pathway to end coal consumption all together.

Professor Bordoff, however, bases his argument to the rapidly falling costs of renewables and energy storage. An IEA report from 2021 found that renewables are the most affordable energy option in most regions of the world, and Bordoff notes that solar is projected to reach cost parity with coal in India sometimes next year (after which point the cost of solar will continue to fall while coal costs may rise). He also notes the challenge of high cost of capital for developing countries, and puts the onus on developed countries to follow through on their commitments and provide accessible capital for clean energy projects to support growth.

[1] Based on this investment, BP anticipates production to reach 2.3 million barrels of oil equivalent per day by 2025 before reducing to 2.0 million by 2030 (a 25% reduction from 2019 production levels).

[2] “Transition growth engine” investment will be split roughly in half between established businesses in bioenergy and convenience and EV charging, and growing businesses in hydrogen, renewables and power (including targeting a global “position in offshore wind).