What we can learn from South Africa's energy crisis

Plus the problems with the Energy Charter Treaty, global mining giants embracing the energy transition, lithium mines and carbon pipelines in the US, and a useful explainer on US-Europe natural gas.

(View of the massive Oyu Tolgoi copper-gold mine in Mongolia, recently acquired by mining giant Rio Tinto Source: Bloomberg)

This week we look at two warning signs in the operation and transition of the energy sector: first, how highly concentrated, state-owned power providers (a common model around the world) are especially at risk from systemic corruption. And second, the role outdated treaties and international agreements can play in hindering the clean energy transition. We also look at how the global mining sector is adopting a notably different direction from its oil major counterparts by investing heavily in serving the clean energy transition. Finally, two key updates on U.S. decarbonization sectors: lithium supply and carbon capture pipelines.

Learning from South Africa’s Energy Crisis

DRIVING THE NEWS: South Africa’s energy crisis has continued to deteriorate, with the electricity system currently operating at less than 50% of its installed capacity and March 5th marking the 64th day of rolling blackouts this year (Bloomberg). The blackouts are estimated to cost as much as $51 million per day according to the South African Reserve Bank.

WHY IT MATTERS: South Africa has a unique situation in which nearly all of its power is provided by the highly centralized state owned utility, Eskom. This has left the utility highly susceptible to issues of corruption and hindered the ability of the provider to meet the needs of its customers–providing a case study of the perils of state-owned power provider monopolies “in a system where corruption is endemic” (Washington Post).

THE CONTEXT: South Africa has been dealing with an extended domestic energy crisis for years, and the situation is complex. On February 9th, President Cyril Ramaphosa declaring a state of emergency as rolling blackouts continued to worsen and an ongoing dispute between the president’s African National Congress party and outgoing Eskom CEO André de Ruyter escalated.

The problem with power blackouts, however tracks as far back as 1998 when a white paper was first published showing that electricity demand would outstrip supply by 2007. Despite the warning, the government invested little into building more energy infrastructure. This has resulted in a fall in per capita electricity consumption and is a major driver in stalled growth of GDP per capita.

THE ROLE OF CORRUPTION: Corruption continues to be a major issue in the power sector, with a presidential investigation launched last December and the National Defense Force deployed to generating plants to deal with sabotage, theft and graft.

De Ruyter claims that his removal as CEO is in response to him pointing out endemic corruption including the presence of criminal syndicates that he claims have been stealing coal and equipment from the utility. To add to the intrigue, two months ago De Ruyter survived an attempted poisoning which he says was “indeed an attempted murder, not just a warning” (Financial Times).

A September 2022 report from the Global Initiative Against Transnational Organized Crime found that, “South Africa’s infrastructure is suffering from sustained and organized theft, mainly of copper, on an industrial scale affecting the transport, energy, water, communication and fuel sectors… This has eroded state capacity to provide critical services.” South Africa is currently ranked 72 of 180 on Transparency International’s Corruption Perceptions Index, which is similar to India and China.

LOOKING FORWARD: At this point, no quick fix for the electricity supply issues seem to be available. New coal plants would take roughly 10 years to build (based on South Africa’s construction history) and switching to other sources takes time. Fortunately, the case for solar has gotten much strong as prices have fallen, and a new focus on decentralized grid infrastructure (includes microgrids for remote electrification) will help going forward.

DIVE DEEPER: For an in-depth report on the situation facing Eskom, CEO André de Ruyter, and the South African government, take a look at this Financial Times investigation.

Recognizing the Importance of the Energy Charter Treaty

THE CONTEXT: The Energy Charter Treaty (ECT) is a little-known agreement enacted in April 1998 to promote energy cooperation through international law. The treaty includes 53 Signatories and Contracted Parties largely from Europe, the Middle East and Central Asia (Japan is also a signatory).

The ECT provides protection for foreign investments in the energy sector (particularly coal, oil, gas and nuclear), allowing companies and investors to sue states through international arbitration. The ECT was originally designed to promote Western investment in energy infrastructure in post-Soviet countries by offering legal protection to investors (Investigate Europe provides deep dive on the history and features of the ECT).

THE ARGUMENT: In a recent opinion piece published in the Financial Times, former UK Energy Minister (and current HKS M-RCBG Senior Fellow) Chris Skidmore explores the negative impact that ECT is having on the energy transition and argues that the UK should follow its “like-minded” partners to begin the process of withdrawal.

The ECT provides an avenue for fossil fuel companies to sue governments for introducing climate policies. In 2022, Italy was sued for €190 million for enforcing its ban on offshore oil drilling–six times the plaintiff’s original investment in the project. Lawsuits have also been brought against the Netherlands for its coal phaseout plans and Slovenia for its ban on fracking.

European countries including Germany, France, Spain and the Netherlands have already decided to leave the treaty given its inconsistency with being able to meet Paris Agreement goals. This leaves the UK with a weakened coalition to be able to put forward modernization proposals for the treaty when the member countries meet to discuss reforms in April.

WHY IT MATTERS: The chief concern raised by Skidmore is that these lawsuits will have a “chilling” effect on governments enacting climate policy, right at a time when ramping up such policy is critical to meeting climate targets.

Global Mining Sector Positions for the Energy Transition

KEY TREND: Global mining firms are taking action to align their future businesses with the needs of the energy transition, particularly to deliver on the growing demand for copper, nickel, lithium, and cobalt.

Wood Mackenzie estimated last October that $23 billion in annual investment is needed over the next 30 years just to secure the copper resources needed to reach 1.5ºC target (a 64% annual spending increase over the last three decades).

A more recent story from Market Insider noted that a quarter of the mining sector’s top 20 mergers in 2022 where in direct response to the energy transition.

WHY IT MATTERS: The positioning illustrates the mining industry’s conviction that production of energy transition materials is lagging behind a growing demand, and that these materials are set for a bigger demand boom in the future than traditional industrial commodities of iron and coal. This perspective has sparked major investments in the sector and a commitment to growing the raw materials industry in the coming years (Wall Street Journal).

DRIVING THE NEWS: Mergers and acquisitions within the sector have been on rise as small- and medium-size firms look to grow and mining majors such as BHP, Rio Tinto and Glencore seeking to secure access to energy transition materials.

Rio Tinto, which last December completed a $3.1 billion acquisition of Turquoise Hill Resources that includes gaining ownership over the Oyu Tolgoi copper mine in Mongolia, has announced a goal to double its copper output by 2030. “I certainly think we are fully aligned with that view that the world needs more materials, and we’re upping our game against that, and at the right time,” said Peter Cunningham, Rio Tinto’s CFO.

BHP continues to pursue a $6.6 billion acquisition of OZ Minerals, which would provide the giant with improved access to copper and gold resources. The purchase was approved by Brazilian officials last month and now is waiting on approval from an Australian court and OZ Minerals’ shareholders (Reuters).

The major mining companies have also decided to keep more cash on hand to potentially support new investments–a shift from last year when the sector seemed to be prioritizing dividends and stock buybacks.

In the shorter term, however, major mining companies remain focused on supply to the recovering Chinese market. Both BHP and Rio Tinto are banking on a strong recovery of the Chinese economy, particularly the real estate sector (one of the biggest end consumers of Australian iron ore for steel making).

THE CHALLENGE: The time from resource discovery to full-scale production in the mining sector remains a major challenge to meeting the needs of the energy transition. “Even if something gets found in this year, it’s going to take somewhere between 10 and 20 years to bring that on, depending on which jurisdiction it is,” said Mike Henry, BHP’s CEO.

IEA Convenes First Finance Industry Advisory Board

DRIVING THE NEWS: The IEA held its inaugural meeting of the Finance Industry Advisory Board, which brought together 40 representatives from leading energy finance institutions including banks, asset managers, and international financial institutions.

Fatih Birol, IEA Executive Director: “Successful and secure energy transitions depend not just on policy decisions and technological innovation, but also the mobilization of huge amounts of investment capital – especially for clean energy projects in emerging and developing economies… This is a very dynamic area and I’m very pleased at the strong interest from the energy finance community in this new IEA initiative.”

WHY IT MATTERS: One of the key priorities of the advisory board is to “provide an institutional channel for dialogue between the energy finance community and energy policy makers”. As governments look to accelerate the energy transition and the energy finance community seeks to identify emerging trends and investment opportunities, promoting dialog between the two will play an important role in fostering a coordinated approach.

U.S.’s Thacker Pass Lithium Mine Breaks Ground in Nevada

DRIVING THE NEWS: Last week construction of the Thacker Pass mine, led by developer Lithium Americas Corp., began in northern Nevada (E&E News). The project had been the subject of extended legal battles until a judge finally ruled that the project could move forward last month (Reuters).

The project is expected to produce over 80,000 tonnes of battery-quality lithium carbonate annually, roughly equal to the country’s current demand.

WHY IT MATTERS: The project has been considered by many to be a test of whether the U.S. can in fact approve and develop large-scale mining projects for energy transition materials. The project received strong bipartisan and federal support, and will ultimately serve to help transition the U.S. in part away from dependence on foreign suppliers.

Sen. Catherine Cortez Masto (D-Nev.) said, “we are the only state with the critical minerals necessary to support our nation’s clean energy economy, and I have worked across the aisle to strengthen this supply chain and make sure Nevada businesses and working families benefit as it continues to grow.”

Republican Governor Joe Lombardo’s office added that Nevada is, “positioned to be ground zero for the energy transition and to play a key role in securing the energy independence and security of the United States.”

THE GEOPOLITICS: This project builds on the trend of countries around the world seeking to secure their critical material supply chains as the energy transition unfolds. The chief concern is that if current material supply chains persist (which rely largely or entirely on Chinese extraction and production), dependent countries will be exposed to the risks of geopolitical pressure similar to today’s oil producers.

The U.S. has been pursuing a number of high priority projects to increase domestic lithium and other transition material supply chains, but progress has been slow as local environmental and other concerns have hindered project progress.

Note that this project is separate from the Rhyolite Ridge Lithium-Boron project also located in Nevada, which is being developed by Ioneer and which received a DOE LPO conditional loan in January.

CO2 Pipeline Regulatory Questions

WHY IT MATTERS: U.S. companies looking to develop thousands of miles of pipelines in the coming years for transporting captured CO2 are running into issues around the question of who should be regulating these projects.

THE ARGUMENT: It is unclear under current federal regulations whether the Department of Transportation’s Pipeline and Hazardous Materials Safety Administration (PHMSA)–which oversees natural gas pipeline regulations–automatically has similar jurisdiction over CO2 pipelines (E&E News).

Safety advocates argue that natural gas pipelines being converted to carry CO2 are not covered by current regulations, and that existing standards for transporting CO2 for enhanced oil recovery purposes do not cover new pipeline projects. Many organizations are pushing for a moratorium on the construction of new projects until new federal regulations are complete.

Pipeline companies are arguing that the PHMSA has clear jurisdiction over such projects and that construction should be allowed to go ahead under that assumption.

State agencies are left waiting for confirmation about whether PHMSA will regulate the new pipelines, with many sending requests to the agency and other simply stating that they are preempted by federal law and will assume that PHMSA will take jurisdiction.

PHMSA has begun to examine its rules and draft new regulations for carbon pipelines, but is not expected to release a draft until October 2024 at the soonest. A 2020 CO2 pipeline failure in Satartia, Mississippi caused the regulatory body to strongly reconsider current regulations and has formed the bases of the new rulemaking process (PHMSA).

THE GEOPOLITICS: Pipelines are a key component of the carbon capture supply chain that the U.S. and other countries hope to build in the coming decades. Major funding around the world has been dedicated to various forms of carbon capture. But moving the gas from the point of capture to storage or utilization facility will require a new network of pipelines. As a leader in the growing carbon capture industry, delays due to regulatory questions in the U.S. could have ripple effects that slow the growth of the sector globally.

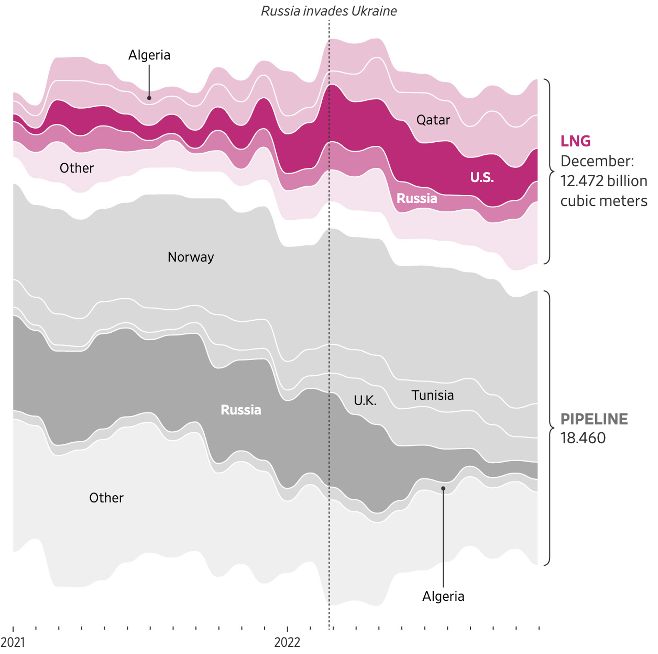

Explainer: The Natural Gas Supply Chain, from U.S. to Europe

This week the Wall Street Journal published an in-depth look at the natural gas supply chain from the wells in Texas, Louisiana, and Appalachia to end users in Europe. While most of the information in this story is likely review, I did want to highlight one statistic and two interesting graphics:

First, the piece notes that the monetary cost of losing Russian gas supply to the EU will be at least $315 billion in infrastructure through 2030. This includes both temporary costs such as leasing floating storage regasification units, and the more permanent infrastructure needed to transition supply chains.

Second, this chart shows the EU’s monthly natural gas imports by source for both LNG and pipeline gas. I found this to be a very helpful summary of how the supply has shifted since the start of the energy crisis and the role different supply countries are playing the new Europe energy mix.

(Source: Wall Street Journal)

Third, this map of LNG ships that visited U.S. ports between June and December 2022. This illustrates the key American LNG import points in Europe.

(Source: Wall Street Journal)